Investment information - agreements and conditions

Here you will find everything about agreements and conditions in connection with investing through Jyske Bank.

In connection with your advisory basis, your risk capacity and risk profile will be assessed based on the following basis

We must inform you about all forms of consideration, including commission, which we receive from our business partners.

No Jyske Bank employee receives commission or bonus from Jyske Bank or from any of our business partners.

Here you find information about how to calculate market value, market risk and credit risk.

Calculation of risk on derivative financial instruments [PDF]

You should always contact your branch in case you are dissatisfied with your relationship with Jyske Bank or if you are dissatisfied with the outcome of any inquiry.

If, after having discussed the problems with your branch, you do still not agree with Jyske Bank, you may file a complaint with: Jyske Bank A/S, Juridisk Afdeling, Vestergade 8-16, 8600 Silkeborg. See more information

If you still disagree with Jyske Bank, you may submit a complaint to: Pengeinstitutankenævnet Østerbrogade 62, 4. sal, 2100 København Ø, tel.: +45 35 43 63 33 - www.pengeinstitutankenaevnet.dk

You should submit your complaint using a special form which is available from the Danish Complaints Board of Banking Services and can be downloaded from the Board’s website listed above. The Complaints Board currently charges DKK 150 for hearing a complaint. The amount will be refunded if your complaint is sustained in part or in full, or if your complaint is rejected, withdrawn or lapses.

Business Policy – Designated Publishing Entity (DPE)

Purpose

A DPE (Designated Publishing Entity) is an investment firm that makes any financial instrument transaction to which it is a party public through an APA (APA | Finanstilsynet) – when the transaction is governed by a duty of publication.

Investment firms can choose in which classes of financial instruments it wants to be registered as a DPE.

Scope

Jyske Bank has opted in as DPE (Registrering som udpeget offentliggørelsesenhed | Finanstilsynet) in the following classes of financial instruments

- Equities

- ETFs (Danish investment certificates)

- Depository receipts

- Certificates

- Other similar financial instruments

- Bonds

- Interest-rate derivatives

This means that the bank will make public any transaction between you and the bank in any of the above-mentioned financial instruments, unless you are registered as a DPE yourself. In this case, the bank will only make a transaction public, to which the bank is the selling party.

On the contrary, the bank has not opted in as DPE in the following classes of financial instruments:

- ETCs (Exchange Traded Commodities)

- ETNs (Exchange Traded Notes)

- Structured financial instruments

- Emission allowances

- Credit derivatives

This means that the bank only has a duty to make any transaction in the above-mentioned financial instruments between you and the bank public, if the bank is either the selling party, or the transaction has been made with a client classified as either a retail client or a professional client who is not themselves registered as an investment firm.

Transactions between the bank and an investment firm (which is not bound by a duty of publication) will no longer be made public by the bank, unless the bank is the selling party.

Publication of Commercial Policy

This Commercial Policy is available at Jyske Bank's website: jyskebank.dk/investeringsinfo. The Policy is regularly updated.

The Terms and Conditions of Custody Accounts include the terms and conditions applying to custody accounts with Jyske Bank unless otherwise expressly agreed with the Bank. Find the terms and conditions here.

Financial products’ consideration of EU criteria for environmentally sustainable economic activities. According to Regulation (EU) 2019/2088 (“Disclosure Regulation”), financial products must be categorized according to their approach to sustainability.

"Article 9 products" are products having sustainable investments as their goal.

"Article 8 products" are products marketing environmental and/or social characteristics.

"Article 6 products" are all other products which cannot be categorized as Article 8 or Article 9.

Financial products at Jyske Bank, which are not individually in each agreement categorized as an Article 8 product or an Article 9 product, are categorized as an Article 6 product.

According to Regulation (EU) 2020/856 (”Taxonomy Regulation”), we are obliged to inform you that the investments underlying these Article 6 financial products do not take into account the EU criteria for environmentally sustainable economic activities.

Click on this link to see the stock exchanges and financial institutions with which Jyske Bank does business.

Jyske Bank excludes in its asset management activities a number of companies for investment as appears from the sections about norm- and activity-based screening in the Jyske Bank Group's policy on responsible and sustainable investment

We pursue a zero-tolerance policy with respect to investments in companies relating to weapon types violating international conventions ratified by Denmark. All companies with this type of products will be placed on the exclusion list. Furthermore, investing in a number of companies that in other ways violate the principles for norm- and activity-based screening may be blocked.

A number of mandates with special sustainability considerations will have additional exclusion criteria.

See the complete exclusion list [PDF]

Rules of coverage with effect from 1 June 2015

Garantiformuen covers amounts deposited on accounts with financial institutions up to the equivalent of EUR 100,000 (approx. DKK 750,000) in the event that the financial institution goes bankrupt.

If you have loans with the same financial institution that have fallen due for payment, the amount owed by you will be deducted from your deposits before you receive coverage from Garantiformuen.

Deposits which pursuant to legislation have social objectives e.g. industrial injury compensation or personal injury compensation or compensation from Lønmodtagernes Garantifond etc. (see the full list at www.finansielstabilitet.dk) are covered up to EUR 150,000 (approx. DKK 1 million) for a maximum of six months as from the date at which they were deposited on the account.

Deposits as a result of transactions relating to real property which have in particular been used or should be used for purposes other than commercial purposes will be covered up to an amount equivalent to EUR 10 million (approx. DKK 75 million) for up to 12 months as from the time when the amount was deposited on the account.

Deposits on pension accounts are fully covered without limitation.

Who is covered?

Garantiformuen covers personal and corporate clients.

In case of more account holders of an account, these are regarded as several depositors. Deposits on the account are shared between the account holders and included in the calculation of the amount guaranteed for every depositor by Garantiformuen.

Certain special client types, including public authorities and financial companies, are not covered by Garantiformuen.

Securities

The bankruptcy proceedings of a financial institution will not affect the delivery of securities held in own custody accounts, e.g. at the Danish Securities Centre. If the financial institution cannot deliver the securities, Garantiformuen will cover up to EUR 20,000 per investor.

What is not covered?

Garantiformuen does not cover guarantee obligations, cheques, and securities – including shares, capital notes, guarantee certificates and bonds – issued by the financial institution itself.

Special deposits made before 1 June 2015

Special deposits are also covered without limitation after 31 May 2015, but only by the balance on the account as at 31 May 2015. For pension accounts, however, also deposits made after 31 May 2015 are covered without limitation.

Therefore, you must be aware that if you have, for instance, opened a child savings account, only the balance on the account as at 31 May 2015 will continue to be fully covered. Deposits on the account after 31 May 2015 are covered as ordinary deposits.

Special deposits include for instance "Børneopsparing" (child savings accounts), "Etableringskonti" (establishment accounts), "Skifteretskonti" (probate court accounts), "Forvaltningskonti" (asset management accounts), "Uddannelsesopsparing" (education savings accounts) and "Boligopsparing" (housing savings accounts).

Trust funds deposited on client accounts of attorneys-at-law as at 31 May 2015 are fully covered until the time when the trust funds can be paid out or transferred.

What to do if payments are to be made from Garantiformuen?

Immediately after the bankruptcy of the financial institution you will be given general information about the bankruptcy proceedings, and you will as soon as possible receive a list of the total amount owed to you by the financial institution and instructions describing how to proceed.

Additional information

Read more about Garantiformuen's rules of coverage at www.fs.dk or contact your usual relationship manager.

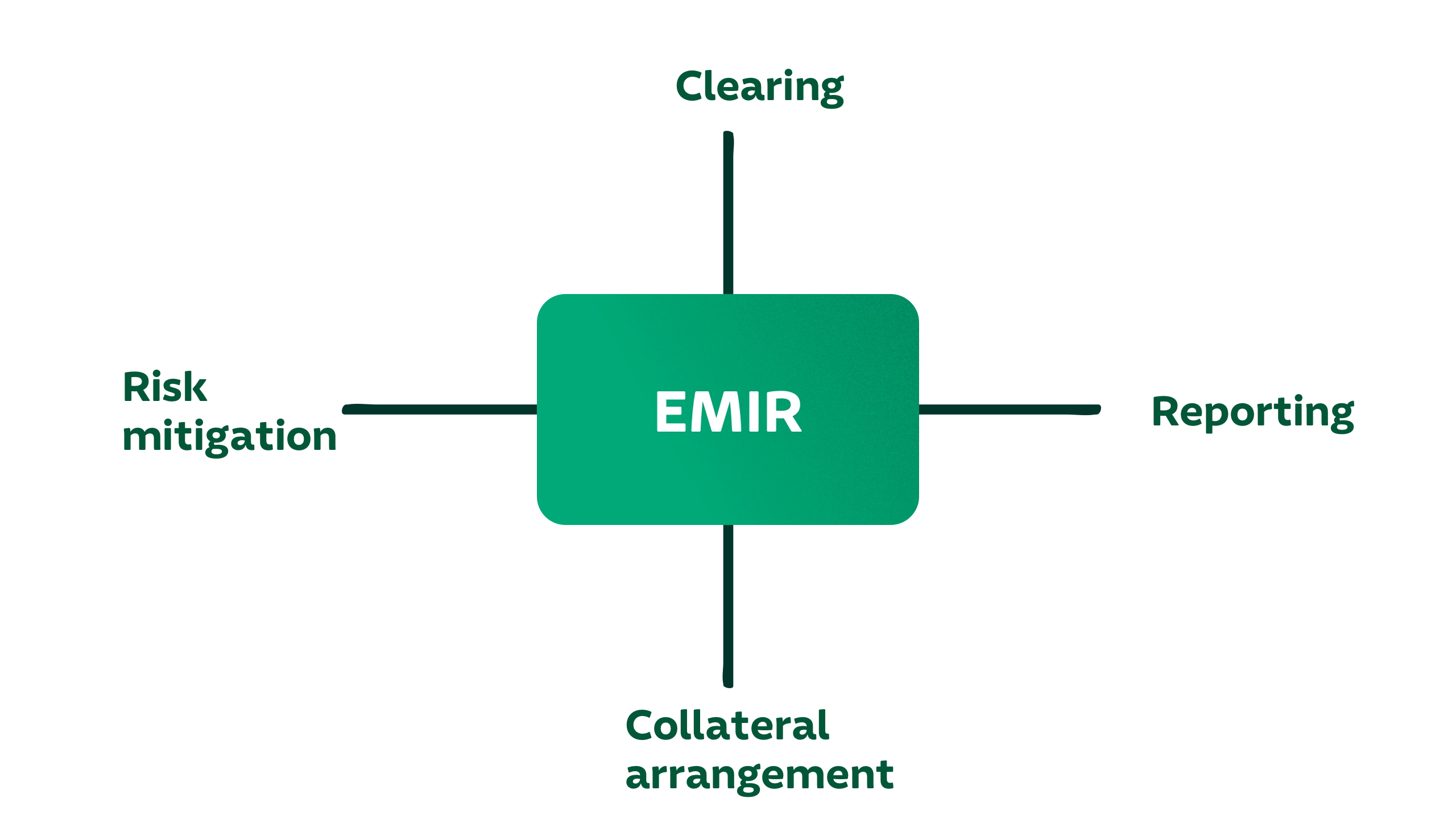

Rules for trading in derivative financial instruments

In 2009, the G20 countries adopted a resolution of which the purpose is to prevent a new financial crisis as a consequence of failure to manage the risk on derivative financial instruments, hereinafter termed derivatives. In Europe, the resolution is implemented, among other things, under the European Market Infrastructure Regulation (EMIR).

EMIR imposes various different obligations, of which the most important are illustrated in the chart.

The various obligations in the risk mitigation, clearing, reporting and collateralisation area depend on the company’s client and counterparty category.

EMIR distinguishes between five client and counterparty categories:

- Financial counterparties (FC)

Banks, insurance companies, investment firms and other parties that are subject to the clearing obligation. - Financial counterparties (FC-)

Financial counterparties that are not subject to the clearing obligation. - Large non-financial counterparties (NFC+)

Companies with a volume of derivatives that exceeds the thresholds in the respective categories, and which are therefore subject to the clearing obligation. - Small non-financial counterparties (NFC-)

Companies and business operators with a volume of derivatives that does not exceed the thresholds in the respective categories, and which are therefore not subject to the clearing obligation. - Private individuals

Private individuals who trade derivatives under their own Danish personal registration number.

The client and counterparty category influences whether, and to what extent, the respective rules under EMIR are of significance to the company, and how they are to be applied.

Calculation of status as NFC- or NFC+

A status as NFC- gives significant administrative savings. It is therefore a requirement to provide annual verification that the conditions for NFC- status continue to be met. This takes place by calculating the current trading volume in various categories of derivative trades and comparing this to the thresholds stated under EMIR.

If the company does not wish to make the calculation, it will be considered to have NFC+ status in accordance with EMIR. The status of NFC+ entails that the company is subject to the clearing obligation, and that the company itself must report its derivative trades.

Since the thresholds for the transition from NFC- to NFC+ are relatively high, and the cost and administrative savings are considerable, most Danish companies will be interested in making the calculation in order to retain the NFC- category status.

Derivatives with the following characteristics must be included in the calculation:

- Traded “over the counter” (OTC) and not on an exchange, for example.

- Transactions that are not intended to limit commercial risks and are therefore of a speculative nature.

- Active, not yet expired transactions.

- Intragroup transactions are included in the calculation.

The calculation is made by:

- Allocating the derivative trades to the following categories.

- Adding up the gross nominal value of all derivative trades in each category.

- The sum of the gross values in each category is compared to the following thresholds.

As of 18 June 2020, the following thresholds apply to the individual derivative types:

- Credit derivatives: equivalent of EUR 1,000,000,000

- Equities derivatives: equivalent of EUR 1,000,000,000

- Fixed income derivatives: equivalent of EUR 3,000,000,000

- Currency derivatives: equivalent of EUR 3,000,000,000

- Commodities derivatives: equivalent of EUR 3,000,000,000

See the current thresholds at https://www.esma.europa.eu/post-trading/clearing-thresholds.

The bank does not know the companies’ and any intragroup transactions with other counterparties and therefore cannot make the calculation.

Clearing obligation

- Financial counterparties (FC)

FC are obliged to clear all derivative trades that are subject to the clearing obligation (see current overview [PDF]), and not only in the categories that are exceeded, if the company has a volume of active derivative trades in one or several categories that exceed the aforementioned thresholds.

A company that is not subject to the clearing obligation is categorised as FC-. - Non-financial counterparties (NFC)

NFC are obliged to clear their derivative trades in the category(ies) that are exceeded, and if they are subject to the clearing obligation they are categorised as NFC+. NFC- are not subject to the clearing obligation.

The advantage of clearing is that the company does not have different claims and obligations, arising from derivative trades, in relation to different counterparties.

By using a clearing house for settlement of derivative trades, you can net various offsetting claims and reduce the risk for all parties.

If your company is subject to a clearing obligation, the required contractual and technical measures must be taken in good time.

Reporting obligation

EMIR imposes a reporting obligation on the bank and all clients. However, Private individuals trading derivatives under their own Danish personal registration number are exempt from the reporting obligation.

Jyske Bank is obliged to make reporting for the clients categorised as NFC- clients. As an NFC- client you may, however, inform Jyske Bank in writing if you wish to make the reporting yourself. NFC+ clients are obliged to report their derivatives transactions to a transaction register themselves. To ensure that the supervisory authorities may access trade data. As an NFC+ client you may, however, enter into a written agreement with Jyske Bank to the effect that Jyske Bank makes reporting on behalf of the client and itself.

All derivative trades must be reported to an approved transaction register.

For Jyske Bank to be able to report correctly on a client's behalf, the client must have a LEI code, and enter into a reporting agreement. The reporting agreement is a supplement to the existing agreement on trading in derivative financial instruments.

All companies subject to the reporting obligation must have a LEI code. The LEI code is an international code for identification of companies that trade in derivatives. See more about LEI codes on the Danish FSA's website (in Danish).

Jyske Bank’s LEI code is: 3M5E1GQGKL17HI6CPN30

If the client chooses to report its derivative trades itself, these trades must be identified by the UTI (Unique Trade Identifier) assigned by Jyske Bank.

Jyske Bank’s UTI codes will usually have 42 digits, with the following structure:

(10 digits: QGKL17HI6C) + (10 digits: digits 7-16 of the client's LEI code) + (4 digits: Year of the trade) + (18 digits: Trade ID from the confirmation, including characters with preceding zeros).

EMIR statutory requirements concerning collateral arrangements and risk mitigation

Financial counterparties (FC/FC-) and non-financial counterparties (NFC+) that exceed the thresholds are obliged to have risk management procedures that require timely, accurate and appropriately segregated exchange of collateral with respect to OTC derivative contracts.

The exchange of collateral consists of two types of margin:

- Variation margin

Must protect the parties from value fluctuations related to the market value at any time of the established, non-cleared OTC derivative contracts. - Initial margin

Must be provided on the establishment of a non-cleared OTC derivative contract and be subject to ongoing adjustment. Its purpose is to protect a party from potential losses that may arise in a closure situation during the period between the last exchange of variation margin and until the OTC derivative contracts have been replaced or their risks equivalently hedged.

The requirement for the exchange of collateral solely applies to new, non-cleared OTC derivative contracts that are entered into on or after the date of entry into force of the margin requirement.

There are a few conditional exemptions from and deferrals of the requirement for the exchange of collateral in relation to certain contracts – see more on the Danish FSA's website.

Notification of status changes to the bank

Any change of status from NFC- to NFC +, or vice versa, must immediately be notified to the bank. After any change of status from NFC- to NFC+ the bank may still handle reporting on behalf of the NFC+, although this will require a separate agreement.

Reconciliation of trades

EMIR also sets the requirement that the terms for all ongoing derivative trades and their valuation be reconciled at least once a year. However, if more than 100 trades have been made between the client and the bank the requirement is at least once per quarter. If the client disagrees with the terms or the calculated market value, the client must notify the bank, so that the parties can come to an agreement.

At Jyske Bank, this reconciliation takes place at the end of the year or quarter.

On a daily basis, Jyske Bank sends an overview of existing derivative trades between the client and the bank, with details of calculated market values, to the client's online banking mailbox.

Resolution of disputes

There must be agreed rules for handling disputes. Jyske Bank's terms are that the client must check the confirmation of the trade before it is signed. The client must also check the daily overview of calculated market values. If the client disagrees, the client must contact their adviser at the bank. If the client cannot reach agreement with the adviser, the client must send a written complaint by email to [email protected]

More information

For further information about EMIR, see the Danish FSA's information about EMIR (in Danish).

Shareholder rights

What is the Shareholder Rights Directive?

The EU has issued a directive that will expand the rights of European investors. The directive covers the shares of companies with domicile in the EU and if the share has been admitted for trading within the EU. Investment certificates are in this respect not regarded as shares and are therefore not covered. The directive has been implemented in national legislation.

Purpose of the directive

The intention is to create a closer link between the companies that issue shares and the shareholders who buy the shares. The aim is to encourage shareholders to exercise their rights while ensuring that the necessary conditions are in place to make this possible.

This means that every time there is a corporate event, this information must be communicated from the issuer to the shareholders. Returns information about changes in the share ratio, various offers and settlement notes will be distributed unchanged.

By law, shareholders will receive notice of general meetings for all covered shares, both Danish and foreign shares. The announcement is a general announcement that does not include custody account holdings. For shareholders who purchase shares after the notice of general meeting has been submitted, but before the deadline for participation has expired, information will be collected on a daily basis and the latest announcement will be distributed.

How and where does the information come from?

The notification is delivered to your Netboks. If you want to be informed about what's new in Netboks, you can attach a notification in the form of a text message.

How can I vote?

Proxy voting: For Danish shares, shareholders must vote via the Shareholder Portal or the Investor Portal, and it is free of charge.

For foreign shares, shareholders must submit their vote to Jyske Bank's Corporate action team ([email protected]) for registration. This is done against payment of a fee of DKK 1,000. In addition, foreign costs are added. The prices are inclusive of 25% VAT. We also refer to the price book where all fees for the exercise of shareholder rights are stated.

If you do not wish to exercise your rights, they will automatically expire when the deadline expires. If you have any other questions, you are welcome to contact Jyske Bank by phone +45 89 89 73 70 or by email to [email protected].

Jyske Bank has adopted and signed the FX Global Code of Conduct (FXGCC). Hence, we back the unique cooperation between central banks and market participants around the world. The code consists of 55 principles and aims to promote a robust, fair, liquid, open and transparent foreign exchange market.

More information about the FX Global Code can be found below.

At Jyske Bank you can trade the below non-complex instrument categories via self-service channels such as Jyske Netbank and Jyske Mobilbank.

- Equities [PDF]

- Investment certificates [PDF]

- Mortgage bonds [PDF]

- Government bonds [PDF]

- Corporate bonds, simple [PDF]

If you are interested in advisory services concerning these instrument categories, it is a statutory requirement that we make sure that you have knowledge of the instrument categories you want to trade via a relationship manager at the Bank. You may obtain knowledge of the non-complex instrument categories through your relationship manager or your investment adviser.

You may also gain trading access to more complex securities, such as US equities, ETFs, complex corporate bonds, EM bonds, ADR, certificates etc. This only requires that your knowledge of such types of securities is tested. Such testing is a statutory consumer protection measure, cf. MiFID II. If you are interested in trading with complex instrument categories, please call +45 89896999 during 9 am and 5 pm.

Complex instruments

At the Jyske Bank Group, we consider it our primary responsibility, in the best way possible, to optimise the return for our investors. We assume corporate social responsibility in relation to its investments, which means that environmental, social and governance (ESG) issues are taken into consideration in the investment decision process.

The basis of the Jyske Bank Group’s work with responsible investment is UN PRI’s Principles for Responsible Investment (PRI). UN PRI is a joint declaration on taking corporate social responsibility in connection with investments and compliance with six central principles for responsible investments.

Read our policy for responsible and sustainable investment [PDF]

Statement of changes to policy for responsible and sustainable investment [PDF]

The policy describes the Jyske Bank Group’s approach to active ownership. It provides the framework for the Jyske Bank Group’s work on active ownership, including engagement with companies and exercise of voting rights. The policy is a Group-wide policy, which applies when portfolio management or investment advisory services are provided in Jyske Bank A/S within the scope of asset management.

When you trade in financial instruments in Jyske Bank, you must be able to understand and compare the most important aspects and risks of the investment you wish to make. Therefore we are under the obligation to make a number of information documents on financial instruments available to you - PRIIPs key information.

In accordance with the Danish executive order on investor protection in respect of securities trading, we are required to categorise all clients according to the Markets in Financial Instruments Directive (MiFID). MiFID categories determine the degree of investor protection that the client enjoys and which is described under each category.

There are three MiFID categories prescribed by law:

- Retail clients - enjoy the highest level of investor protection

- Professional clients - enjoy a slightly lower level of investor protection

- Eligible counterparties- enjoy no investor protection

In addition, it is possible for retail clients to be categorised as an “elective professional client” for one or more asset classes. This means they will be treated as professional clients in respect of the asset classes for which they fulfil certain criteria.

Retail Client

As a retail client you obtain the highest level of investor protection, which implies, among other things, that:

- you must receive information about our prices and services in good time before you execute transactions

- we must ensure that you have sufficient knowledge or experience in trading in relevant financial instruments (securities)

- before purchasing selected investment certificates and certain other investment products you may request a PRIIPs KID

- when we advise you, we must obtain knowledge about your investment purposes so that we can offer you advice matching your needs including also knowledge about:

- Your educational background

- Your occupation

- Your time horizon and risk tolerance

- Your financial affairs

- advisory minutes (suitability assessment) are prepared every time you have received advisory services and before any transactions are executed

- we are obliged in connection with the execution of orders to obtain the best possible price inclusive of trading costs unless we execute the order according to other criteria determined by you

- every three months we send you a list of holdings

- one every twelve months, we send you a total overview of the amount paid in investment service costs and product costs

All clients who do not fulfil the requirements of being categorised as a professional client or eligible counterparts cf. below will be categorised as retail clients. Retail clients may hence be both personal clients and business undertakings.

Elective professional client in connection with one or more asset classes

Retail clients trading very actively in some types of financial instruments may request re-categorisation as an "elective professional client” in connection with one or more asset classes. This means that in respect of these asset classes, a client can be treated as a professional client even though the client is a retail client. The client has to apply to the bank to be re-categorised as an elective professional client. In accordance with the law, the Bank must make a thorough assessment whether the client is capable of making his own investment decisions and understanding the risks involved. In addition, at least two of the following three criteria must be satisfied:

- the client has carried out transactions, in significant size, in the relevant market – at an average frequency of 10 per quarter over the previous four quarters

- the size of the client’s financial portfolio, defined as including cash deposits and financial instruments, exceeds EUR 500,000

- the client works or has worked in the financial sector for at least one year in a professional position, which requires knowledge of transactions or service envisaged

Seen in relation to the categorisation as a retail client, the categorisation as an elective professional implies lower protection in the form of:

- with respect to information about costs and fees the client and the Bank may agree to give less detailed information

- there is no requirement of the bank to prepare advisory minutes after the provision of advisory services and before any transactions are executed

- before purchasing selected investment certificates and certain other investment products you may request a PRIIPs KID

Per se professional clients

A per se professional client is a large undertaking meeting two of the following three size requirements on a company basis:

- own funds of EUR 2,000,000

- balance sheet total of EUR 20,000,000

- net turnover of EUR 40,000,000

Seen in relation to the categorisation as a retail client the categorisation as a per se professional client implies a lower degree of protection in the form of:

- that the Bank may take its point of departure in the per se professional client having knowledge and experience in trading relevant financial instruments (including securities)

- the Bank may take its point of departure in the client’s financial affairs being sufficient to make the desired investments and understanding the financial consequences of the investments

- there is no requirement that the Bank prepares advisory minutes after the provision of advisory services and before any transactions are executed

- with respect to information about costs and fees the client and the Bank may agree to give less detailed information

- before purchasing selected investment certificates and certain other investment products you may request a PRIIPs KID

Eligible counterparty

The legislation defines eligible counterparties as a specific type of undertaking, for instance: financial institutions, pension funds, insurance companies.

Eligible counterparties only benefit from a moderate degree of investor protection in the form of:

- information on investment services and financial instruments

- information about costs and fees for investment services

- reporting on transactions and services rendered

An eligible counterparty receiving advisory services or portfolio management services is treated in the same way as professional clients.

Jyske Bank will take all reasonable steps to achieve best execution, when executing orders on your behalf.

See a list of the various order types which Jyske Bank offers you.

Jyske Bank has prepared business procedures designed to identify and handle conflicts of interest.

Here is a complete list of the costs of various services at Jyske Bank. At the moment the information is only available in Danish.

Jyske Bank has entered into cooperation agreements with several investment associations, and as we offer advice on their investment products, the bank is not an independent investment adviser. When you own certificates in these investment associations, the bank receives payment (called sales commission) from the association.

The bank receives this commission for making its distribution network available to the association and for offering advice in relation to the association’s certificates.

See here for a comprehensive outline of the bank’s cooperation partners in the area of investment. And gain a full overview of the rates of commission applicable to the various investment association certificates.

Before you buy certificates from an investment association, you will be informed of the annual sales commission applicable to your certificate. You will also receive the annual report “Årlige Investeringsomkostninger” (Annual Investment Costs), which will show the total amount you paid in the form of sales commission.

Quality-enhancing services

When Jyske Bank receives sales commission, the bank offers services to its clients, which will enhance the quality of your client experience when investing. The higher the commission the bank receives, the more services you will be offered.

If you wish to see the stage you are at right now and the quality-enhancing services that you are entitled to, please contact your adviser.

Please note: If you are a private banking client with the bank, you will receive a description of your personally adjusted service and value propositions from your adviser.

Below you find a list of the products for which Jyske Bank is a systematic internaliser and our commercial policy for the area.

Detailed list - Equities, Bonds and Exchange-traded funds [PDF]

Here you can find the statement describing how Jyske Bank A/S takes into account the principal adverse impacts on sustainability factors when providing investment advice:

Report on the principal adverse impacts of investment advice on sustainability factors [PDF]

Here you can find the six most recent annual statements describing how Jyske Bank A/S and relevant subsidiaries take into account the principal adverse impacts on sustainability factors when making investment decisions:

2025: Statement on the principal adverse impacts of investment decisions on sustainability factors [PDF]

2024: Statement on the principal adverse impacts of investment decisions on sustainability factors [PDF]

2023: Statement on the principal adverse impacts of investment decisions on sustainability factors [PDF]

2022: Statement on the principal adverse impacts of investment decisions on sustainability factors [PDF]

2021: Statement on the principal adverse impacts of investment decisions on sustainability factors [PDF]

2020: Statement on the principal adverse impacts of investment decisions on sustainability factors [PDF]

Jyske Bank A/S currently uses The Bank of New York Mellon SA/NV as a custodian for foreign securities.

Here you can read how Jyske Bank integrates sustainability risks in investment advice.

Here you can read how Jyske Bank integrates sustainability risks in our investment decisions.

Foreign dividend tax

Denmark has entered into double taxation treaties with several countries. For some of these countries, we can offer to reduce or claim back the foreign dividend tax. The requirements and rules for documentation change all the time, and therefore the service we can offer will also change.

There are three different schemes. If you are not sure which scheme(s) is relevant to you, please contact [email protected], and we will be pleased to help.

- Foreign securities listed on VP Securities A/S

- Tax services on foreign securities

- US securities

Please note that foreign countries do not distinguish between pension funds and liquid assets; they tax all custody account types equally. Under item 2, a few calculation examples are shown.

1. Foreign securities listed on VP Securities A/S

Danish investors liable to pay tax and who receive dividends from one of the Finnish or Swedish companies held at VP Securities can have their foreign dividend tax on dividend payments reduced.

For Finnish securities, the dividend tax can be reduced from 35% to 15%. For Swedish securities, the dividend tax can be reduced from 30% to 15%. This also applies to custody accounts for pension saving schemes.

To use this service, please contact your adviser who can help you sign up. The service costs SEK 500 per year per custody account that is registered.

2. Tax services on foreign securities

Requires that Jyske Bank is authorized to reclaim foreign dividend tax on your behalf and that the Danish Tax Agency certifies the documents that Jyske Bank must send to other countries.

Sign up via your adviser or by contacting [email protected].

Tax services:

- Can be granted to individuals and companies that are fully liable to pay tax to Denmark

- Generally, only offered on securities held in the country in which they were issued

- Depends on whether the name and address information we have match the information registered with the public authorities.

In the Nordic countries, you can obtain a reduction of foreign dividend tax when paying dividends (reduction at source). This service is currently free of charge. See rates in the table below.

| Home and storage country of the paper | Full tax | Reduced tax |

|---|---|---|

| Sweden | 30% | 15% |

| Finland - Service is currently on hold / under clarification | 35% | 15% |

| Norway | 25% | 15% |

In Germany, Belgium and Switzerland, full foreign dividend tax is paid on dividend payments. Tax can subsequently be claimed back down to 15%. The amount to be reclaimed must have a value exceeding USD 250. We only claim back the tax if there is a net profit. Recovery - DKK 400 + VAT per dividend + foreign costs.

| Home and storage country of the paper | Full tax | Reduced tax |

|---|---|---|

| Germany | 26,375% | 15% |

| Belgium | 30% | 15% |

| Switzerland | 35% | 15% |

Calculation example 1 – Pension funds - tax service Swedish share

Participates in tax service: 15% to Sweden + 15 percentage points discount in PAL tax (i.e. PAL tax of 0.3%) = Total tax of 15.3%

Does not participate in tax service: 30% to Sweden + 15 percentage points discount in PAL tax (i.e. PAL tax of 0.3%) = Total tax of 30.3%

Calculation example 2 – Liquid assets - tax service Swedish share

Participates in tax service: Swedish dividend tax of 15% + Danish dividend tax (27%-15%) of 12% = Total tax of 27%

Does not participate in tax service: Swedish dividend tax of 30% + Danish dividend tax (27%-15%) of 12% = Total tax of 42%

Portugal and Spain – only bonds

Interest tax is reduced for coupon payments if all documentation is in place (reduction at source). Annual fee to cover foreign costs DKK 2,500 per country.

| Home and storage country of the paper | Full tax | Reduced tax |

|---|---|---|

| Spanish bonds Spanish Eurobonds | 19% 0% | 0% 0% |

| Portuguese bonds Portuguese eurobonds | 19% 0% | 0% 0% |

Italian shares

Companies may have their dividend tax reduced from 26% to 1.2%. Specific documentation is required. Contact [email protected], and we will make sure to get the documentation in place. This service is currently free of charge.

Italian bonds

In order to trade Italian bonds at Jyske Bank, you must have an Italian Trade Certificate.

Contact [email protected] and we will help you get it set up. This service costs EUR 100 in foreign costs. The execution time is up to 3 weeks.

3. US securities

In order to reduce the US dividend/interest tax on dividends/interest payments, personal clients must be documented with either a passport or a driver's license. For companies, an extract from the Danish Business Authority and a Declaration of Agreement (reduction at source) must be obtained.

Registration is made via your adviser.

| Home and storage country of the paper | Full tax | Reduced tax |

|---|---|---|

| US equities | 30% | 15% |

| USD bonds | 30% | 0% |

Full terms and conditions

Tax service:

- Follows the standard service offered by our custodian bank abroad on regular dividend and interest payments

- Can be provided to individuals and companies that are fully liable to pay tax to Denmark with the exception of I/S, K/S, P/S and PEV with CVR number

- Generally, only offered on securities held in the country in which they were issued

- Depends on the name and address information we have that match the information registered with the public authorities

Custody accounts existing at the time of registration will be covered by Jyske Bank's Tax Service. If new custody accounts are created at a later date, please state this when registration of enrolment takes place on each individual custody account.

For all countries - with the exception of the US - we need the signed power of attorney and a Certificate of Residence issued by the Danish tax authorities. We will obtain this document upon registration, just as we arrange for the annual renewal with the Danish Tax Agency. Please note that a processing time of up to 2 months must be expected before all documents have been obtained and registered.

Reduction at source is dependent on the Certificate of Residence being in place when the dividend is paid. If this is not the case, Jyske Bank will in certain situations subsequently arrange for recovery of the overpaid dividend tax. Please note that if reduction at source is not possible due to lack of documentation, it will be transferred to the recovery procedure and may fall below the USD 250 limit.

The tax matrix is indicative. Jyske Bank makes reservations for any errors in the matrix and is not liable for any losses incurred in connection with decisions made on the basis of the information. The stated tax rates are applicable as of 1 November 2019. Jyske Bank will always charge foreign costs that we have been charged.

Reduction at source - free of charge

| Home and storage country of the paper | Full tax rate | Tax rate for clients who have signed up for Jyske Bank’s tax service |

|---|---|---|

| Sweden | 30% | 15% |

| Norway | 25% | 0% |

| Finland - Service is currently on hold / under clarification | 35% | 15% |

| USA 1 | 30% | 15% |

| Italy 2 | 26% | 1,2% |

1 Reduction on US tax requires documentation according to US requirements: a) Corporations: Extract from the Danish Business Authority+ Treaty Statement.

2 Tax service on Italy: Only by special arrangement and only granted to companies, write [email protected]

Reduction at the source - Foreign costs: Annual fee per country DKK 2,500

| Home and storage country of the paper | Full tax rate | Tax rate for clients who have signed up for Jyske Bank’s tax service |

|---|---|---|

| Portugal - only bonds3 | 35% | 0% |

| Portugal - eurobonds | 0% | 0% |

| Spain - only bonds3 | 19% | 0% |

| Spain - Eurobonds | 0% | 0% |

3 Tax service on Portugal and Spain: By special arrangement only, write to [email protected]

Recovery - DKK 400 + VAT per dividend + foreign costs

| Home and storage country of the paper | Full tax rate | Tax rate for clients who have signed up for Jyske Bank’s tax service |

|---|---|---|

| Germany4 | 26,375% | 15% |

| Belgium | 27% | 15% |

| Switzerland | 35% | 15% |

4 Tax Service on Germany requires the document “Declaration and Authorization Letter for Electronic Filing Procedure” to be signed.

There is increased focus from both authorities and media on cases where ordinary clients “trade with themselves” on the stock exchange (wash trades), i.e. are both buyer and seller in a trade that takes place on the stock exchange.

This is illegal and is considered market manipulation. This applies regardless of whether the trade is between two custody accounts that you own or for which you have power of attorney. You should therefore be extra careful when trading securities via Online Banking/Mobile Banking where the order is very likely to end up on the stock exchange.

Some cases have ended with severe penalties, which is why we refer to the FSA's warning in July 2022 that you can read below. Please note that you are responsible for complying with the rules on market manipulation.

The FSA’s warning against trading securities with yourself (wash trades)

What can you do to avoid trading with yourself?

If you need to transfer securities between your custody accounts, please contact your adviser who can help you with the process and ensure that you are not doing anything illegal.

Please note that transferring securities between two financial institutions, for example when transferring bank facilities, is not problematic as such transfers are not traded on the stock exchanges.

What can you do to avoid trading with yourself? (Danish Financial Supervisory Authority)